Business Model Innovation in Action: What SANY’s Electric Trucks Mean for European OEMs

This post was inspired by Stef Cornelis, who visited SANY’s electric truck plant in China and shared his first-hand observations on LinkedIn. If you want sharp, on-the-ground insights into the future of electric mobility, follow him — it’s worth it.

One truck every six minutes. That’s the production rhythm at SANY’s electric truck plant in China — the largest of its kind in the world. While European manufacturers debate the pace of electrification, SANY has already settled the question. And now they’re heading to Europe.

This isn’t just an automotive story. It’s a business model innovation story. And the lessons apply far beyond trucks.

From Diesel to Electric in Five Years: A Decision, Not a Roadmap

Five years ago, SANY was a conventional diesel manufacturer. Today, they produce electric trucks exclusively for the Chinese domestic market — roughly 90% of their total volume. That’s not a product update. That’s a complete reconstruction of the business architecture.

European OEMs have spent years arguing that the transition to electric commercial vehicles must be gradual. Regulatory uncertainty, infrastructure gaps, customer readiness — the list of reasons to move slowly is long and familiar. SANY’s story demolishes that logic. But the more important question is: what made the transformation possible at all?

The answer lies in what you might call the fourth element of any business model: the spirit of the enterprise — the values, the culture, and above all, the decisions that leadership is willing to make and stick to. SANY’s leadership made a clear, irreversible call: electric only, domestic market, full speed. That decision ended internal debates about pace and priority. It forced the reconstruction of capabilities rather than the protection of existing ones. Without that decision, nothing else follows. Transformation speed is not primarily a technology problem. It is a decision problem. SANY decided. European OEMs are still deliberating.

The Scale Gap Nobody Wants to Talk About

Here are the numbers that should keep European truck executives awake at night.

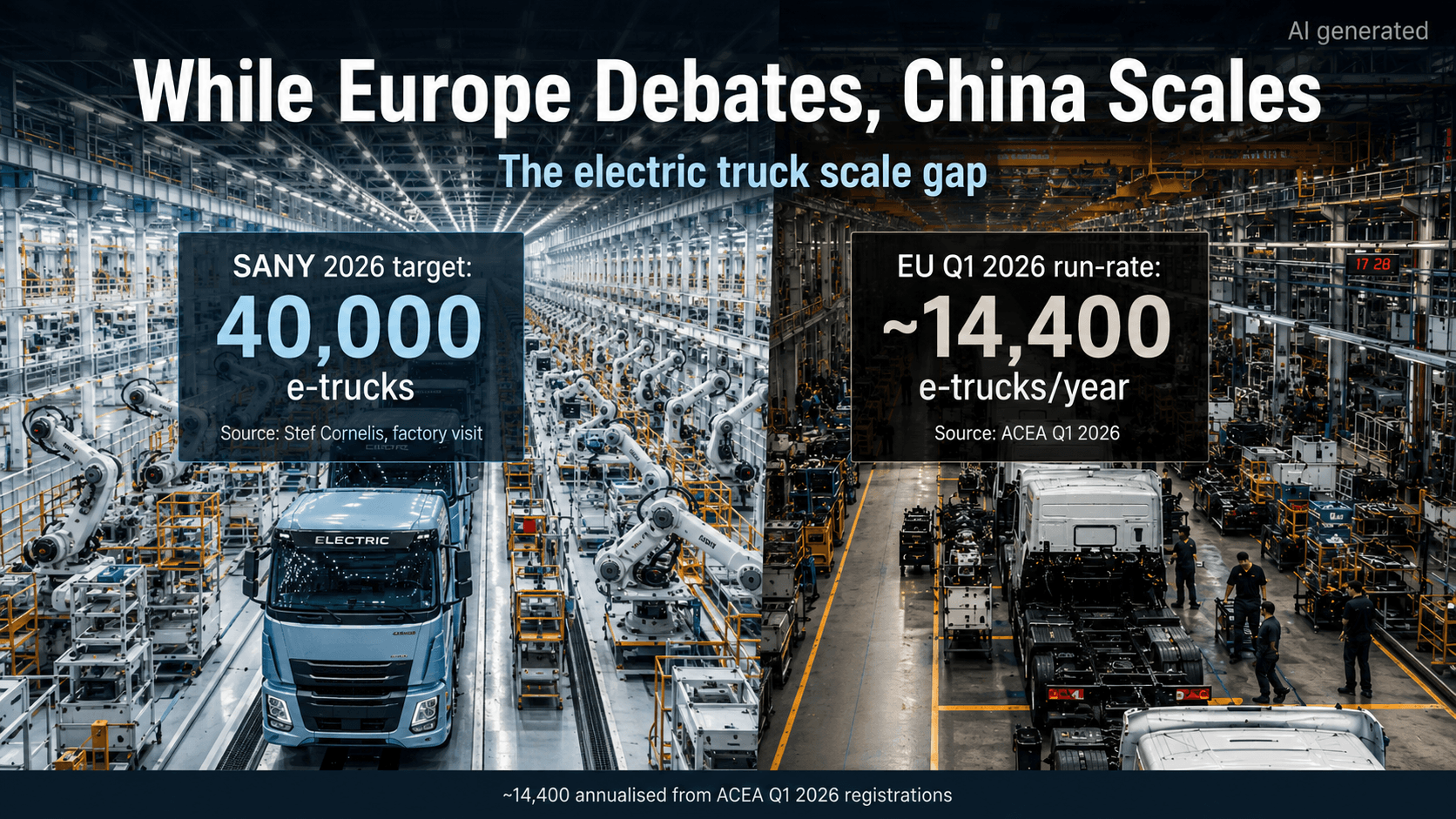

As reported by Stef Cornelis after a factory visit to SANY’s electric truck plant, SANY has already sold around 11,000 electric trucks in China in 2026 and is targeting 40,000 units by the end of the year.

Europe, by contrast, is still operating at a completely different scale. According to the European Automobile Manufacturers’ Association (ACEA), total EU truck registrations reached 81,766 units in Q1 2026, while electrically-chargeable trucks accounted for only 4.4% of the market. That implies roughly 3,600 electric trucks in the first quarter. Annualised, that equals around 14,400 electric trucks for the year — not as a forecast, but as a simple Q1 run-rate.

SANY is therefore aiming for nearly triple Europe’s current annualised pace — alone.

This matters because scale is not just an operational metric — it is the engine of a fundamentally different cost structure. At 40,000 units per year, fixed costs are distributed across a base that makes European volumes look artisanal. Learning curves steepen. Supplier negotiations shift. Per-unit economics improve in ways that engineering talent alone cannot replicate. European OEMs are not on a slower version of the same cost curve. They are on a structurally different one — and closing that gap requires volume commitments that most have not made.

The efficiency trap is real: European OEMs have optimized their diesel businesses to near-perfection. That optimization does not transfer to electric. The most productive diesel plant in Europe is irrelevant to the race SANY is running. Efficiency measures how well you do something — not whether it is still the right thing to do.

A 20% Price Premium — and Falling

Four years ago, SANY’s electric trucks cost three times more than their diesel equivalents. Today, that gap has narrowed to roughly 20%. The trajectory is clear: cost parity is a matter of when, not if.

The mechanism behind this compression is the cost structure that scale enables — not a engineering breakthrough. This is the critical distinction. As long as European OEMs produce electric trucks in small volumes, they cannot close this gap through better engineering alone. The revenue model of premium pricing, built on decades of diesel brand equity, is now structurally exposed. Fleet operators — the actual customers making purchasing decisions — buy total cost of ownership, not badges. A 20% premium is defensible with strong service and brand trust. A credible alternative priced 30% below? Much harder to sell.

Designing for Electric: Why a Clean Sheet Changes Everything

Perhaps the most telling detail from SANY’s factory floor is this: their latest generation trucks were designed from scratch as electric vehicles, not retrofitted from diesel chassis.

The result is a fundamentally different product — and a fundamentally different value-creation architecture. Reduced axle weight. Lighter electric motors. More room for batteries or additional payload. As a SANY representative put it directly: “An e-truck is a fundamentally different product, so why would we use the same design?”

This is the question every incumbent should ask about their own industry. Retrofitting existing product logic onto new technology is faster and cheaper in the short term. It also protects existing production capabilities and avoids writing off past investments. But it produces an inferior product — and it leaves the door wide open for competitors who start with a blank page and build entirely new core capabilities around the new technology.

Apple didn’t make the iPhone by improving Nokia’s best phone. SANY didn’t build their leading electric truck by electrifying their best diesel. The clean-sheet approach is strategically uncomfortable precisely because it requires abandoning what made you successful. It is also, very often, the only path to building something genuinely better.

Europe Is Next

SANY plans to begin selling in Europe next year. The 636 kWh model. And they are confident they can price it well below European OEM equivalents.

Whether that plays out exactly as projected matters less than the direction of travel. A large-scale, cost-competitive Chinese electric truck manufacturer is entering the European market. The question is not whether this creates pressure — it clearly will. The question is what European OEMs do with that pressure.

The honest answer, from a business model perspective, is that most of them are not ready. Their production architectures were built around diesel. Their cost structures reflect low-volume electric production. Their revenue models assume premium pricing that a credible, cheaper alternative will challenge directly.

Even if the European market grows faster in the second half of 2026, the scale gap remains striking. ING Research expects the market share of heavy electric trucks above 16 tonnes in Europe to exceed 5% in 2026, up from around 3% in 2025. The IEA’s Global EV Outlook 2026 confirms the broader pattern: electric truck sales are growing globally, but the decisive momentum is in China, where adoption and scale are already far ahead of Europe.

The service network will be SANY’s biggest barrier — and European OEMs’ last real moat. Fleet operators do not just buy trucks; they buy uptime, maintenance contracts, and roadside support. If SANY can build or partner its way to a credible service network, it removes that barrier. European OEMs should be investing heavily in making their service advantage as strong as possible — because it may be the only sustainable differentiator left.

Five Lessons for Every Business, Not Just Truck Manufacturers

The SANY story is extreme in its numbers. The lessons, however, are universal.

Decisions create speed, not plans. SANY’s transformation happened because leadership made a clear, irreversible call and aligned the entire organization behind it. Endless analysis and gradual commitment produce gradual results — and gradual results in a fast-moving market are just slow-motion losing.

Scale is a strategic weapon, not just an operational goal. Whoever reaches scale first shapes the cost structure of the entire industry. Small-volume producers in a scale-driven market are not just at a price disadvantage — they are structurally locked out of the economics that make competition possible.

Efficiency in the old model is a trap. Optimizing what you have does not build what you need. A business is often most productive right before an innovation makes it obsolete. The perfectly optimized diesel plant is not an asset in an electric world — it is a sunk cost that makes the necessary transition harder to justify.

A new technology deserves a new architecture. Retrofitting old product and production logic onto new technology produces mediocre outcomes and protects capabilities that may no longer be relevant. The clean-sheet approach is harder. It is also the only way to build something that a competitor cannot replicate by simply copying your existing design.

Business model innovation is about the connections, not the parts. SANY’s advantage is not one clever decision — it is the interdependence of all of them. The clean-sheet design enabled a better product. The better product justified volume commitments. The volume commitments created the cost structure. The cost structure built the price advantage. Business model innovation can start anywhere in the system — with a new customer insight, a new production approach, a new revenue logic. But the competitive advantage only becomes durable when the pieces reinforce each other. That is what makes it hard to copy, and what makes it worth building.

The trucks are just the medium. The message is about what happens when a competitor rebuilds their entire business model — deliberately, systematically, from the ground up — while you are still optimizing the one you already have.

Source: First-hand observations and data from a factory visit to SANY’s electric truck plant in China, reported by Stef Cornelis on LinkedIn.